Legal Checklist for Fundraising-Ready Startups (2025 Guide)

This comprehensive 2025 guide offers a complete Legal Checklist for Fundraising to help startups prepare for investment with confidence. From key legal documents like founder agreements, SHA, NDAs, ESOPs, and SAFE vs. convertible notes — to proper incorporation (Private Limited Company), due diligence readiness, IP protection, and common legal mistakes to avoid — we break down everything you need to become investor-ready. Finally, discover how PakLawAssist can simplify and streamline your legal preparation.

Target Audience: Pre-seed to Series A startup founders in Pakistan (or aiming internationally) preparing topitch investors.

Table of Contents

- Why Legal Readiness Matters for Fundraising

- Incorporation Structure: Private Limited Company is a Must

- Founders’ Agreement and Equity Split

- Shareholders’ Agreement (SHA) and Term Sheets

- Non-Disclosure Agreements (NDAs) and IP Protection

- Employee Stock Ownership Plan (ESOP)

- SAFE vs Convertible Notes: Choosing a Fundraising Instrument

- Cap Table Management and Ownership Records

- Investor’s Legal Due Diligence Checklist

- Common Legal Mistakes Startups Make (and How to Avoid Them)

- Final Thoughts: Building a Legally Solid, Investor-Ready Startup

Why Legal Readiness Matters for Fundraising

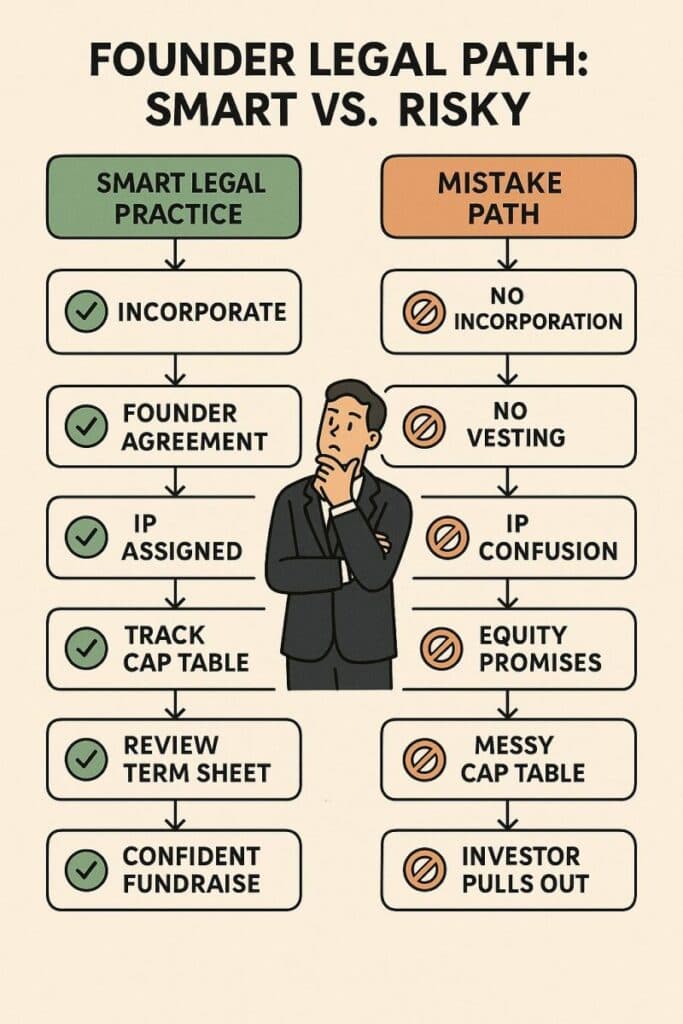

Before you approach any angel or VC, ensure your legal house is in order. Investors perform thorough due diligence and legal missteps can derail a funding deal. For example, issues like unassigned IP or a messy equity structure can scare off investors. In fact, “from unfiled IP assignments to poor cap table management, many common legal mistakes startups make can derail fundraising efforts or lead to long-term governance issues”.

Getting your legal documents ready early shows investors that you’re serious and organized. It helps avoid delays later and makes it easier for them to say yes.

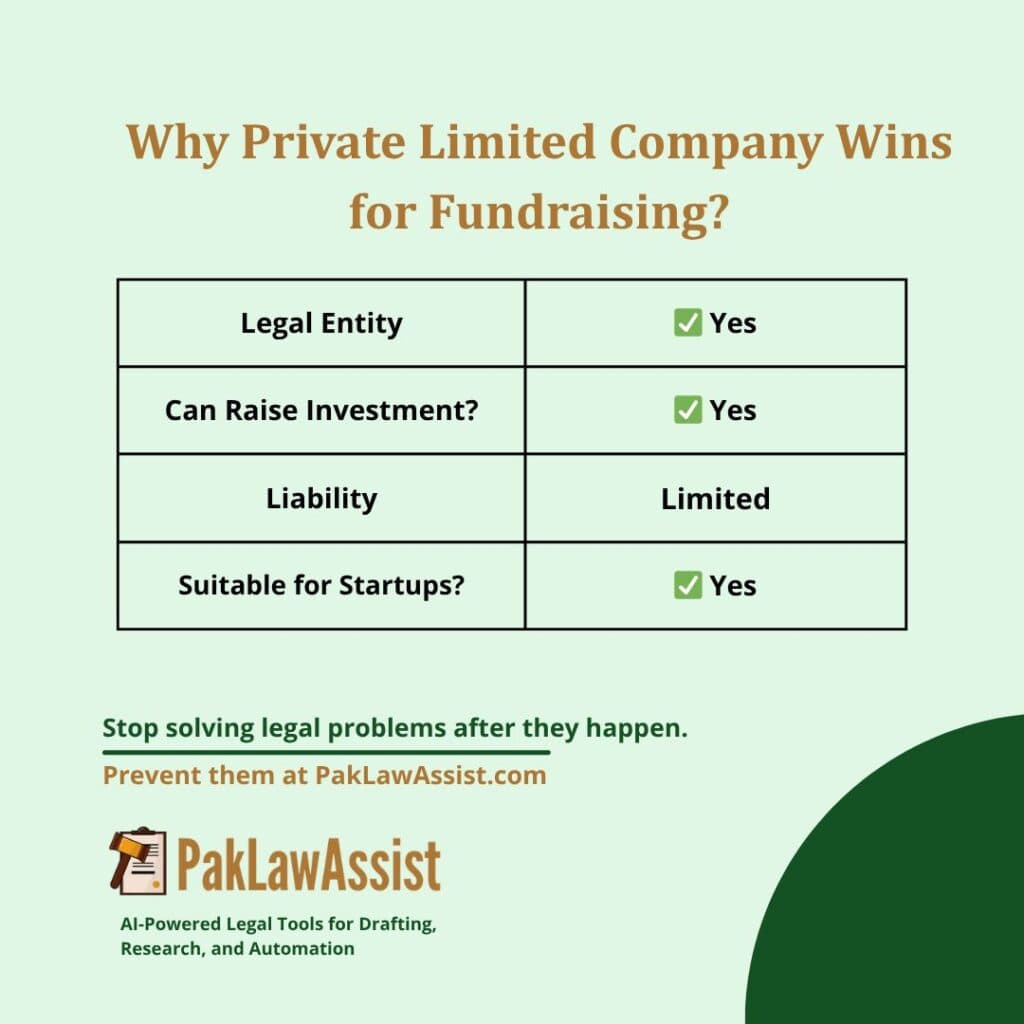

Incorporation Structure: Private Limited Company is a Must

One of the first steps is choosing the right business entity. In Pakistan and most jurisdictions, a Private Limited Company is the recommended structure for startups seeking investment. Unlike a sole proprietorship or partnership, a private limited company is a separate legal entity with limited liability, and it can issue shares to multiple shareholders (which is exactly what investors need). Most venture investors require their target to be a formal company so they can receive equity in return for funding. Other structures (like general partnerships or unregistered businesses) simply aren’t built for equity investment.

Learn how to set up a Private Limited Company in Pakistan in our detailed 2025 guide for startups.

Why “Private Limited”? In Pakistan, private companies cannot invite the general public to buy shares, but they are perfect for startups, allowing a few founders/investors to own the company. This structure limits owners’ personal liability and creates a clear share ownership structure. The Securities & Exchange Commission of Pakistan (SECP) has also been encouraging startup activity – for example, SECP explicitly allows private companies to raise capital even in exchange for non-cash assets or services. This flexibility underscores that the private company is the vehicle through which fundraising happens. Operating as an informal setup or an improper entity is a common mistake that can complicate funding.

Tip: Incorporate early. Ideally, register your startup as a private limited company with at least two directors (or a Single Member Company if solo) well before you start issuing shares or taking investor money. Early incorporation ensures all founders get their shares from the start and you avoid messy ownership disputes later. It also helps in opening corporate bank accounts, registering for tax (NTN), and complying with any relevant laws from day one. If you plan to raise international venture capital, you might eventually set up a holding company abroad (e.g. a Delaware C-Corp or Singapore entity), but you will still likely need a Pakistani private limited operating company for local business. In all cases, having a registered company is non-negotiable for serious fundraising.

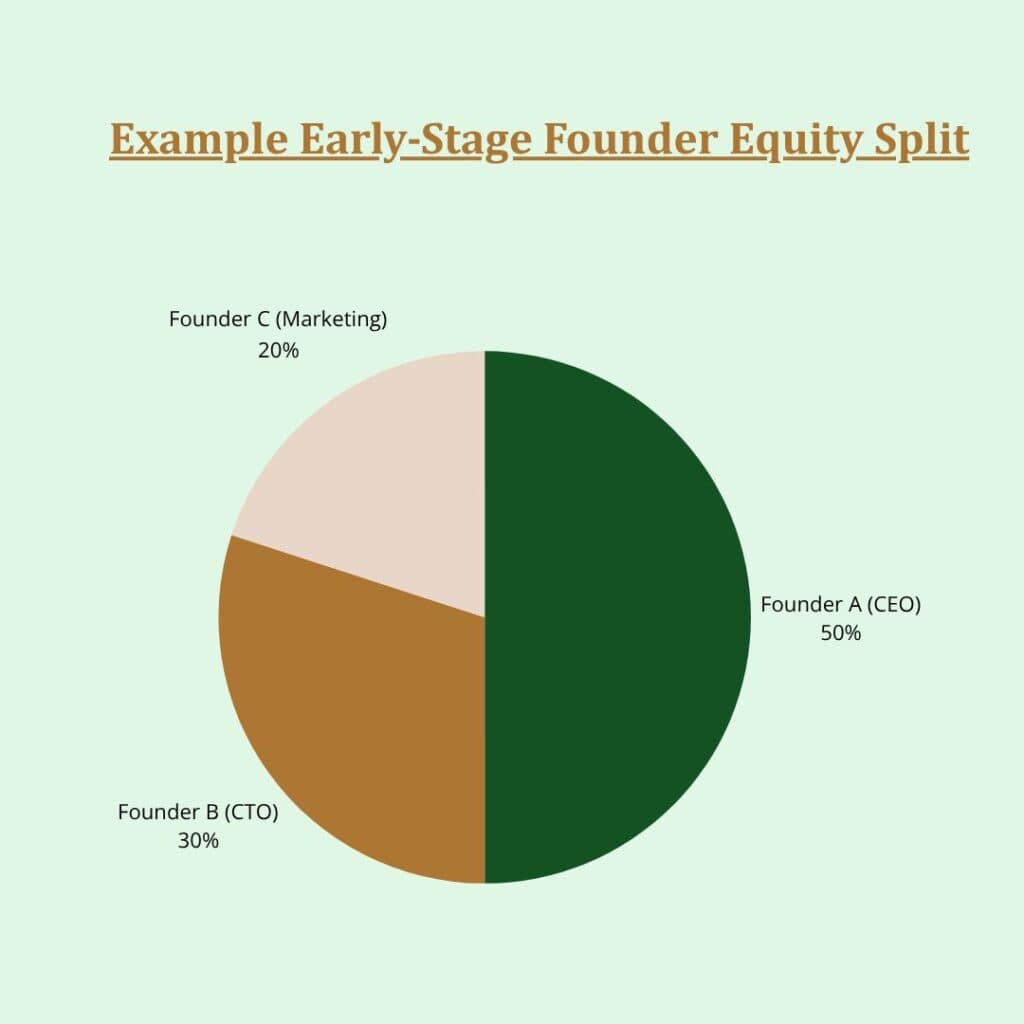

Founders’ Agreement and Equity Split

Before approaching investors, founders must be aligned among themselves. A Founders’ Agreement (or a founders’ Shareholders’ Agreement if the company is already formed) is essential for defining each founder’s equity split, roles, responsibilities, and exit arrangements.

Investors will require that founder shares be subject to vesting…

It’s far better to have any tough conversations with co-founders early:

- How will equity be divided?

- What if someone leaves?

- How are decisions made? than to leave it ambiguous and risk a fallout during due diligence.

A good founders’ agreement typically covers:

- Equity Ownership & Vesting: How much of the company does each founder own, and are their shares subject to vesting? Investors often insist that founder shares vest over time (commonly over 4 years with a 1-year cliff). Vesting means a founder doesn’t fully earn all their shares unless they stay with the startup for a set period. This prevents a scenario where a co-founder owns a large chunk but quits early. “Venture investors will require that all founder shares be subject to vesting… if founders aren’t locked in, the startup’s value proposition is diminished, making fundraising very difficult”. In practice, implementing a vesting schedule (e.g. 25% vest after 12 months, then monthly vesting for 36 months) in your founder agreement or stock issuance documents can assure investors that the founding team is committed.

- Roles & Decision-Making: Outline who is CEO or in charge of what, and how key decisions (strategic pivots, spending, adding new partners) will be made. This can prevent conflicts later and give investors clarity on the leadership structure.

- Founder Departures & Transfer of Shares: The agreement should address what happens if a founder wants to leave or sell their shares. Typically, you’d include right of first refusal (remaining founders or the company get first chance to buy shares) and possibly drag-along/tag-along rights to manage share transfers. Also specify if departing founders lose unvested shares (tying back to vesting).

- Dispute Resolution: It’s wise to agree on mechanisms to resolve disputes (e.g. mediation, arbitration) and define what counts as cause for removing a founder, etc., while everyone is on good terms.

Investors will definitely ask if you have a founders’ agreement in place. Not having one is a red flag. It could lead to nasty disputes right when you’re trying to close a deal.

Imagine an ex-cofounder claiming a large equity share just as a VC is about to invest – a situation that can kill the deal.

Thus, get a solid agreement drafted. Instead of relying on generic templates, you can register your startup on PakLawAssist to access a comprehensive library of legal drafts tailored specifically for Pakistani founders — including detailed co-founder agreements, equity split structures, and more.

If you haven’t yet, draft and sign a co-founder agreement as part of your legal checklist – it’s often cited as one of the “top 5 legal mistakes startups make… failing to create a clear, written Founders’ Agreement” (and one that is easily avoidable).

Non-Disclosure Agreements (NDAs) and IP Protection

Startups thrive on unique ideas and know-how, so protecting confidential information is key.

A Non-Disclosure Agreement (NDA) is a simple but important legal document used to protect sensitive information when you share it with others (whether investors, potential partners, contractors, or employees). An NDA creates a legal obligation for the recipient to keep specified information confidential and not misuse it.

Before fundraising, prepare a standard NDA template for your startup. You might use it when dealing with consultants or vendors or in early discussions with a strategic partner.

However, note on investors: Most venture capital investors will not sign NDAs at the pitch stage. It’s nothing personal – VCs see hundreds of pitches and don’t want potential liability of NDAs. As TechCrunch and other startup advisors note, asking a VC to sign an NDA is generally a bad idea. Instead, protect your sensitive information by patenting critical inventions or only sharing what’s necessary. For example, you can tease your secret sauce in a pitch without giving away the full algorithm until later in due diligence (and even then, there are ways to disclose in stages).

That said, use NDAs for others like any third-party you bring in early (designers, developers, advisors) before sharing detailed business plans or code. Ensure employees and contractors also sign IP assignment agreements alongside NDAs, so that any intellectual property they create belongs to the company (more on IP in due diligence below).

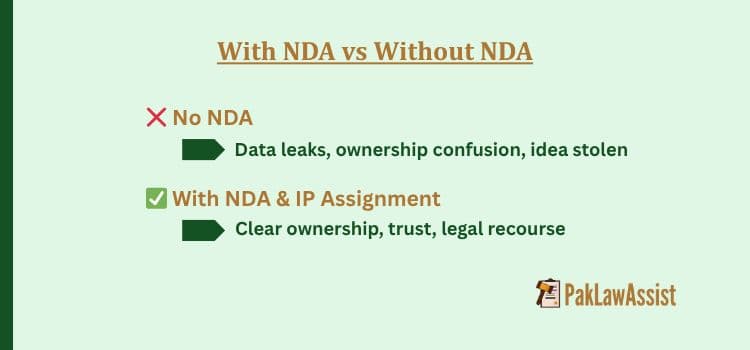

An NDA won’t stop every leak, but not having one invites risk. – PakLawAssist Insights

PakLawAssist makes it easy to protect your startup’s secrets. Instead of relying on generic NDA templates, startups can use PLA’s legally-sound, Pakistan-tailored NDA and IP Assignment Agreement drafts — ready to customize and share in minutes. These legal drafts include all the key elements: clear definitions of confidential information, permitted uses, duration (typically 2–3 years), and standard legal exceptions (like info already public or independently obtained).

| When to Use an NDA? | |

|---|---|

| Investor Pitch | No NDA |

| Strategic Partner | NDA Recommended |

| Contractor/Developer | NDA + IP Assignment |

| Advisor/Mentor | NDA (if sharing business plans) |

| Fundraising Due Diligence | NDA (optional, staged) |

While no NDA can fully guarantee confidentiality, using well-drafted agreements through PakLawAssist acts as a strong legal deterrent — and more importantly, shows investors and partners that your startup takes IP protection seriously from Day 1.

Employee Stock Ownership Plan (ESOP)

As you grow, you’ll want to attract and retain talented employees by offering them a stake in the company. This is usually done through an Employee Stock Ownership Plan (ESOP) – essentially creating an option pool of shares set aside for employees (and sometimes advisors). An ESOP allows employees to earn stock options, which give them the right to buy shares at a fixed “strike” price after they’ve vested.

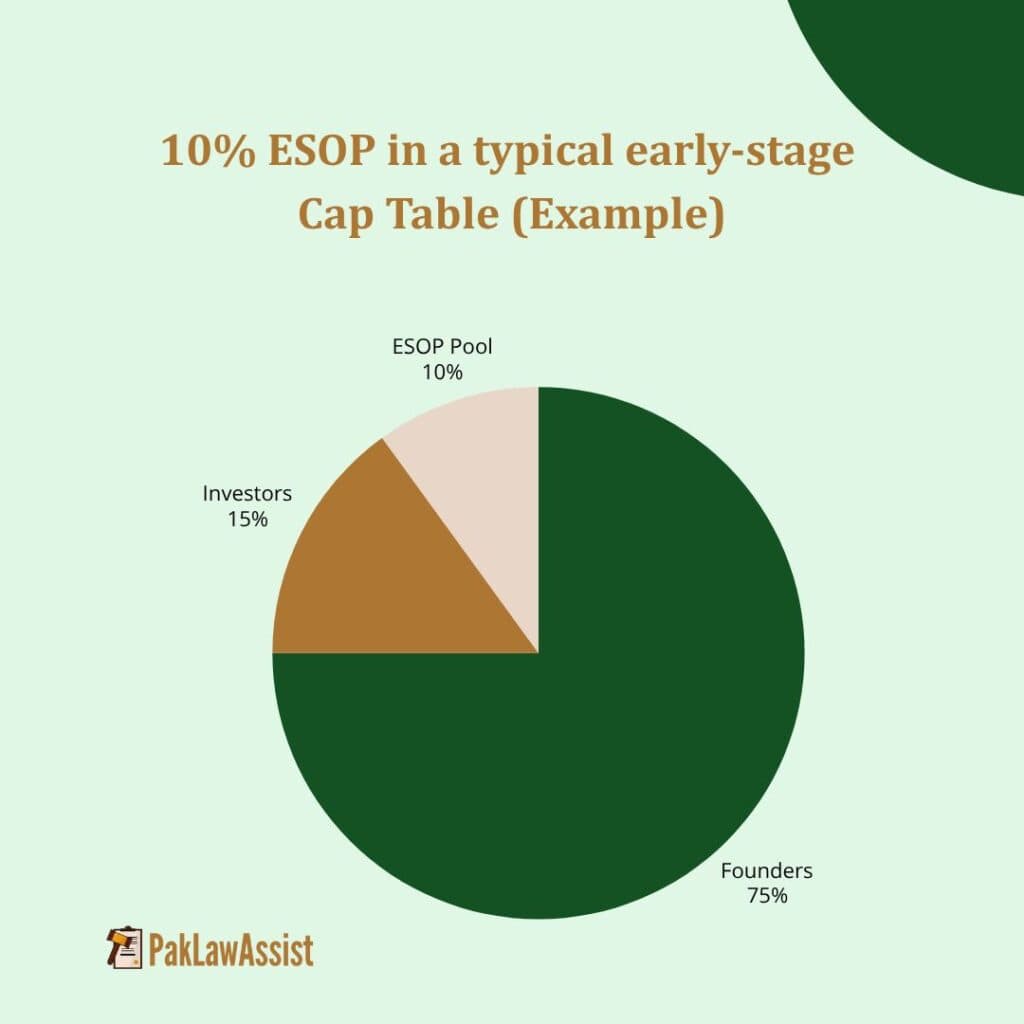

It’s wise to set up an ESOP early, typically around your first funding round if not before. Investors often expect a startup to have, say, a 10–15% option pool reserved in the cap table for current and future hires. In fact, many term sheets will require you to create a certain size ESOP pool before the investment (so that the dilution is borne by founders pre-investment). For example, if you only have 2% set aside and the investor wants a 10% pool, you may need to allocate additional shares to the pool (diluting founders) as a condition of the round. Plan ahead and discuss with investors.

Tip: Without a defined ESOP, you risk sudden founder dilution later. Plan early to protect everyone’s interests.

What does an ESOP entail legally? At a basic level:

- Board & Shareholder Approval: You need board and shareholder approval to create an ESOP and issue stock options. Typically, you amend your Articles or company charter to create an option pool (authorized but unissued shares).

- ESOP Plan Document: This outlines the terms of the plan – who administers it (usually the Board), the total pool size, standard vesting schedule for options (often 4 years with 1-year cliff, like founder vesting), how exercises work, etc. You might have standard agreements that each option holder (employee) receives, stating their grant amount, vesting, strike price, etc. Employee Option Vesting Timeline Year 1: 25% vests after cliff Year 2-4: Remaining 75% vests monthly/quarterly

- Employee Option Vesting Timeline Year 1: 25% vests after cliff Year 2-4: Remaining 75% vests monthly/quarterly

- Year 1: 25% vests after cliff

- Year 2-4: Remaining 75% vests monthly/quarterly

- Market Valuation: If you were a U.S. C-Corp, you’d get a 409A valuation to set a fair market value for the stock (to price the options). In Pakistan, you’ll need to set an exercise price – typically at par value or a fair value – and ensure compliance with any tax rules on issuing underpriced shares. Consult local advisors for compliance (e.g. any approval needed from SECP for share issuance to employees, or tax implications).

Why does ESOP matter for fundraising? Investors view a well-structured ESOP as positive – it means you have a plan to incentivize your team. It also means the equity distribution shown to them is realistic; you won’t suddenly need to dilute everyone to give your CTO some shares later because you’ve planned for it. A startup without an ESOP might worry investors that the team isn’t properly incentivized or that a dilution bomb is waiting to happen.

From a founder’s perspective, an ESOP is how you compete with larger companies for talent – you offer ownership upside.

As Accion’s startup guide notes, “founders and early investors create an ESOP by setting aside a percentage of shares to be granted to future employees” . These shares vest over time for each employee (using a vesting schedule similar to founders).

For example, you hire an engineer and grant them stock options equal to 1% of the company, vesting over 4 years – they’ll need to stick around to earn that full amount, aligning their interests with the startup’s success.

Action items: Work with a PakLawAssist team to draft an ESOP plan and the board resolutions needed. Decide on the pool size (common range 10–15%). Ensure all key early team members sign Option Agreements (and also IP assignment agreements) when they join. Keep track of how much of the pool is granted vs remaining. This will also show up on your cap table (often as “Options Reserved”).

And remember: granting options is a regulated process – in some jurisdictions you might need to file certain forms or pay stamp duty on option grants, etc. Check local regulations (e.g. in Pakistan, ensure adherence to any SECP guidelines on share-based compensation if applicable). A well-run ESOP is a sign of a mature, well-advised startup.

SAFE vs Convertible Notes: Choosing a Fundraising Instrument

In early-stage fundraising, many startups raise money through convertible instruments rather than straight equity. The two popular instruments are Convertible Notes and SAFEs (Simple Agreement for Future Equity). It’s important to understand both, as using them incorrectly can lead to legal and cap table headaches.

Let’s break them down:

- Convertible Note: Essentially a short-term debt that converts into equity in a future round. The investor loans money to the startup, with an understanding that instead of being paid back in cash, the loan will convert into shares when the startup raises a priced equity round (Series A, for example). Convertible notes have an interest rate (e.g. 5% per annum) and a maturity date (by which if no equity round has happened, the note holder could demand repayment or conversion at a given formula) . They often include a valuation cap (the max price at which the note will convert to equity) and/or a discount (e.g. 20% cheaper than the next round’s price) to reward the early investor. In essence, a note is a debt instrument that carries interest and a due date, but it is expected to turn into shares later.

- SAFE (Simple Agreement for Future Equity): A SAFE is not a debt instrument; it’s a contractual warrant or right to future equity. Y Combinator introduced SAFEs in 2013 as a simpler alternative to notes . SAFEs do not have interest or maturity dates – the investor’s money will convert to equity in a future round whenever that happens, but if the company never raises a round, the SAFE doesn’t come due (it’s essentially a perpetual right to convert in the future) . SAFEs typically have a valuation cap and/or discount similar to notes, to set the conversion price advantage for the SAFE investor. Because there’s no interest or deadline, SAFEs are founder-friendly in the sense you don’t have to worry about accruing debt or a looming repayment . They are very popular in seed fundraising now (used by thousands of startups). “Almost all YC startups and countless non-YC startups use SAFE as the main instrument for early-stage fundraising”.

Key Differences at a Glance:

- Instrument Type: Convertible Note = debt (loan); SAFE = not debt (equity contract).

- Maturity Date: Note = Yes (e.g. 18–24 months usually) ; SAFE = No maturity (converts whenever next round happens, no expiry).

- Interest: Note = Yes (accrues interest until conversion or repayment) ; SAFE = No interest.

- Conversion: Both convert to equity at the next priced round (or other triggering events, e.g. acquisition). Both can have valuation caps and discounts to define conversion price.

- If Company Fails: With a note (debt), theoretically the noteholder could claim assets in liquidation (often notes are unsecured, but they stand ahead of equity in bankruptcy). With a SAFE, since it’s not debt, investors typically only get money back if an acquisition happens (sometimes SAFEs have a provision that if the company is sold before conversion, they get either their money back or some defined return). If the company simply folds, SAFE holders often get nothing (similar to equity holders). YC SAFEs have specific language for what SAFE holders get if the company is acquired or dissolves before conversion.

| Convertible Note | SAFE | |

|---|---|---|

| Instrument Type | Debt (Loan) | Equity Contract |

| Maturity Date | Yes (e.g. 2 Years) | None |

| Interest | Yes (Accures) | No Interest |

| Legal Status | Loan Agreement | Investment Contract |

| Risk Profile | Investor may recover funds if startup fails | Investor loses funds if startup fails |

| Common Use Cases | Short-term Bridge Rounds | Pre-seed/Seed Fundraising |

Which one should you use? It depends on investor preference and your situation:

- SAFEs are simpler (usually 5-page document) and don’t require negotiating interest or maturity. They’re great for quick rounds, e.g. raising small checks from angels. Many investors in Silicon Valley prefer SAFEs for seed deals due to their simplicity.

- Convertible Notes are more common if the investors want the structure of a loan, perhaps as a psychological safety or because it’s more traditional. Some investors might insist on a note if they want the option of pulling out at maturity or earning interest. Notes might also be necessary in jurisdictions where SAFEs aren’t legally tested – but in Pakistan and many countries, SAFEs are increasingly used (just ensure you use a jurisdiction-appropriate template – Y Combinator provides versions for certain countries like Singapore, etc. which may be more relevant if you incorporate abroad).

Ultimately, both SAFEs and Notes postpone the valuation discussion to the next round. They help you raise money faster and cheaper (no need to negotiate a full Series A valuation and shareholder rights for a small raise). They’re “fast and affordable: fewer terms to discuss means less time negotiating and lower legal fees” . But be cautious: raising a lot via SAFEs/notes can cause unexpected dilution later if they convert at a low valuation . Always keep track of how these will convert on your cap table (you should ideally model the conversion scenarios).

Action Items: Decide which instrument suits your raise. If using a SAFE or note, get a solid template (Y Combinator’s SAFE template is the gold standard ; many law firms offer note templates as well). Make sure you understand the terms (cap, discount, MFN, etc.) and fill them in carefully. Keep a record of all SAFEs/notes you issue – you will need these in due diligence and to update the cap table.

Side note: If you do a priced equity round instead (selling shares directly), then you’ll be using a Share Subscription Agreement and Shareholders’ Agreement as discussed earlier. Equity rounds are more complex but give finality to valuation and ownership immediately. Many pre-seed/seed deals globally now favor SAFEs/notes for simplicity, but by Series A you’ll almost certainly do a priced round.

Cap Table Management and Ownership Records

Your capitalization table (cap table) is a fundamental document for fundraising. It’s essentially a ledger of who owns what in your startup – listing each shareholder (founders, investors, employees with options, etc.), the number of shares they hold, and their percentage ownership. Keeping an accurate, up-to-date cap table is critical. Investors will request to see it, and any confusion here can spook them.

An example of a post-seed capitalization table: founders hold the majority (60%), an early investor holds 30%, and a 10% ESOP pool is reserved for employees.

A cap table is usually maintained as a spreadsheet (or using specialized software like Carta, CapTable.io, etc.). It should reflect all equity events: founder share issuances, option grants, SAFE or note conversions (on a pro forma basis), and new investor shares.

As AngelList’s education center puts it, “a cap table is a spreadsheet that breaks down who owns what in a startup. The cap table is a key due diligence item because it reveals how every stakeholder is impacted by a fundraise.”

In other words, the investor will scrutinize it to see the current ownership and how their investment will dilute existing holders.

Key elements to track on a Cap Table:

- Authorized Shares: How many shares the company is authorized to issue (set in your incorporation docs).

- Issued (Outstanding) Shares: How many have been issued to people (founders, investors, etc.).

- Share Classes: Common vs Preferred stock (after an investment, you may have separate classes for investors with preferences).

- Each Shareholder’s Holdings: List each stakeholder, how many shares they have, and what percentage that represents. Include founders, each investor, and aggregate any small holders.

- ESOP Pool: Include the reserve for stock options, showing what’s allocated vs available.

- Convertible Securities: List any SAFEs, notes, or warrants separately, including details like their cap/discount, so it’s clear what they could convert into. (These usually aren’t in the main ownership percentages until they convert, but you might provide a pro forma cap table showing percentages if all SAFEs/notes converted at the cap, for transparency.)

- Post-money projections: When raising, often you’ll share a cap table before and after the new investment, so the investor can see their resulting stake and everyone’s dilution.

Common Cap Table Mistakes (to avoid):

- Inaccuracy: Not updating the table after each change. This can lead to major confusion or even legal issues (e.g. two people think they both have 5% because you promised equity informally – avoid by formalizing and recording everything).

- Not accounting for all instruments: Forgetting to include a SAFE or note. This is dangerous – those will suddenly dilute everyone upon conversion. As one legal advisor warns, missing convertible notes or SAFEs in the cap table is a common error that can cause “confusion, valuation disputes, and failed closings.” Always reconcile and double-check the cap table before an investment closes .

- Over-complexity: Having too many small shareholders (from very early sweat equity promises, etc.) can complicate your cap table. Try to keep it streamlined – if you want to reward an advisor or early team member, consider using the ESOP options (so they appear in the option pool) rather than issuing tiny stock slices to many people.

- Failure to update official records: Remember that issuing shares often requires board approval and perhaps filing with regulators (for instance, in Pakistan you must notify SECP of allotment of new shares via Form-3 within 30 days). Ensure your legal filings and share certificates match the cap table. Discrepancies between your internal cap table and official company register are a huge red flag in diligence.

Using modern cap table management tools or at least a well-organized spreadsheet can save you from headaches. Share the updated cap table with major stakeholders periodically. When heading into fundraising, prepare a version that shows the impact of the new investment (this is sometimes called a pre-money and post-money cap table view). Investors will appreciate the clarity.

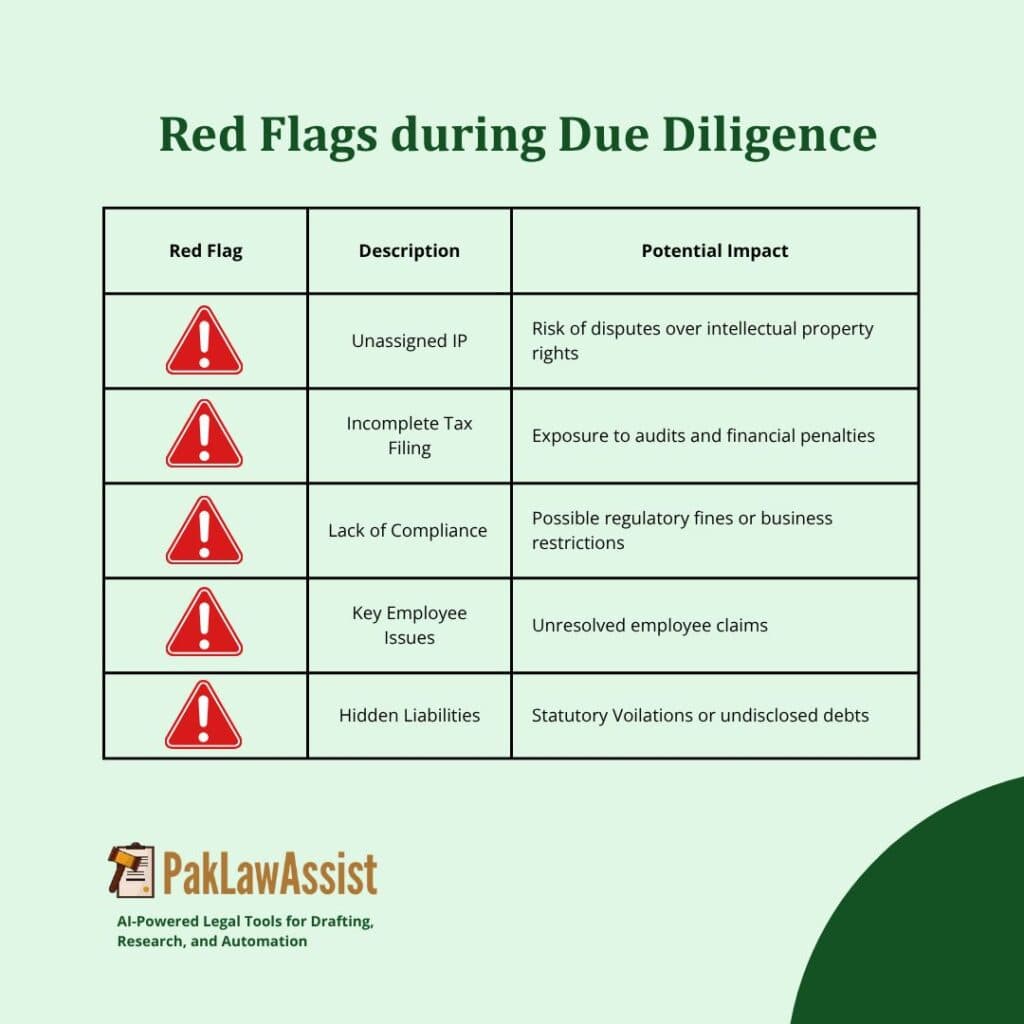

Investor’s Legal Due Diligence Checklist

When an investor is interested and you enter serious talks, they will initiate due diligence – essentially a comprehensive background check on your startup’s health and risks. Legal due diligence is a big part of this. It can be daunting for first-time founders, but if you prepare a data room with all the necessary documents and information, you can breeze through it. Below are key areas investors will examine (and thus you should check off in your own legal readiness list):

- Corporate Structure & Records: Investors will verify your company is properly formed and in good standing. Be ready to share your certificate of incorporation, Memorandum & Articles/Bylaws, incorporation forms filed with SECP, and any registrations (e.g. with tax authorities). They will also look at your shareholder register and past share issuance or transfer documents. Ensure you have copies of all Board resolutions and shareholders’ resolutions, minutes of board meetings (especially any approving key decisions or option grants). If you have subsidiaries or holding companies, prepare an org chart. Essentially, they want to confirm the company’s ownership and governance is legit and that all prior issuance of shares were done correctly.

- Existing Agreements & Liabilities: Compile all material contracts your startup has: Client or revenue contracts, partnership agreements, MOUs. Vendor or supplier contracts that are significant. Any loans or debt agreements. Founders’ Agreement (as discussed) and any Shareholders’ Agreements. If you’ve raised money previously, include SAFE or Convertible Note agreements or any seed investment contracts. Investors will scrutinize these to ensure there are no hidden clauses that could hurt the company or give someone else too much rights. Leases (if you rent an office) or asset purchase agreements. Basically, any binding agreement the company has signed should be organized and available. They will look for unusual terms or contingent liabilities.

- Client or revenue contracts, partnership agreements, MOUs.

- Vendor or supplier contracts that are significant.

- Any loans or debt agreements.

- Founders’ Agreement (as discussed) and any Shareholders’ Agreements.

- If you’ve raised money previously, include SAFE or Convertible Note agreements or any seed investment contracts. Investors will scrutinize these to ensure there are no hidden clauses that could hurt the company or give someone else too much rights.

- Leases (if you rent an office) or asset purchase agreements.

- Basically, any binding agreement the company has signed should be organized and available. They will look for unusual terms or contingent liabilities.

- Intellectual Property (IP): Does the company own its IP? This is crucial for tech startups. You should have: Patent filings or certificates (if any patents granted or pending). Trademark registrations or applications (for your brand/product names). If software, any proof of code ownership – usually this ties back to founder/employee contracts that assign IP. IP Assignment Agreements signed by founders, employees, contractors – to show all intellectual property created by individuals for the startup has been assigned to the company (preventing any individual from claiming it later). If you used open-source software in your product, ensure you comply with those licenses (investors might ask about this in technical diligence). Any licenses the startup holds or granted – for example, if you licensed technology from a university or another company, have that agreement ready.

- Patent filings or certificates (if any patents granted or pending).

- Trademark registrations or applications (for your brand/product names).

- If software, any proof of code ownership – usually this ties back to founder/employee contracts that assign IP.

- IP Assignment Agreements signed by founders, employees, contractors – to show all intellectual property created by individuals for the startup has been assigned to the company (preventing any individual from claiming it later). If you used open-source software in your product, ensure you comply with those licenses (investors might ask about this in technical diligence).

- Any licenses the startup holds or granted – for example, if you licensed technology from a university or another company, have that agreement ready.

The goal is to convince investors that the startup can freely use and commercialize its product/technology without legal threat. Any lingering question like “does someone else have rights to this code?” or “might you be infringing a patent?” will slow down or kill a deal. As one checklist puts it: “Does the startup own its ideas? Is it free to use them without dispute?.

Ensure trademarks, domains, and even social media handles are secured in the company’s name . If you haven’t filed trademarks for your brand and logo, do it before big publicity (investors might nudge you to). For any third-party IP or collaborations, have agreements in place and disclose them.

- Regulatory Compliance: Depending on your industry, this can range from minimal to extensive. If you’re a fintech, health, or education startup, for example, there may be specific licenses or regulatory approvals required. Be prepared to show you have those or are not violating any regulations. Even generally, investors will check compliance with: Company law filings: e.g. annual returns filed with SECP, tax filings with FBR. Tax compliance: have you filed income tax, sales tax (if applicable) returns? Any outstanding tax notices or liabilities? They don’t want a surprise tax default. Labor laws: if you have employees, are you following relevant labor regulations (like minimum wage, EOBI/SS, etc. in Pakistan)? Usually this isn’t a focus at seed stage, but obvious violations could be a red flag. Data protection and privacy: If you handle user data, are you compliant with any data protection laws (e.g. GDPR if you have EU users, or Pakistan’s PECA or upcoming data protection law)? Environmental or other sector laws: if relevant.

- Company law filings: e.g. annual returns filed with SECP, tax filings with FBR.

- Tax compliance: have you filed income tax, sales tax (if applicable) returns? Any outstanding tax notices or liabilities? They don’t want a surprise tax default.

- Labor laws: if you have employees, are you following relevant labor regulations (like minimum wage, EOBI/SS, etc. in Pakistan)? Usually this isn’t a focus at seed stage, but obvious violations could be a red flag.

- Data protection and privacy: If you handle user data, are you compliant with any data protection laws (e.g. GDPR if you have EU users, or Pakistan’s PECA or upcoming data protection law)?

- Environmental or other sector laws: if relevant.

Essentially, “investor due diligence should confirm the startup adheres to general business regulations (data protection, health & safety, etc.) and any sector-specific rules. Any past issues or investigations should be identified”. If your startup had any legal notices or regulatory warnings, be ready to disclose and explain them.

- Financial & Tax Records: Though this veers into financial due diligence, from a legal standpoint ensure: You have proper financial statements (even if just management accounts for early-stage). Tax registrations (National Tax Number, Sales tax registration if needed) are in place. Past tax returns filed (income tax, withholding tax statements, etc.). Investors don’t want to inherit a tax mess. Cap table reconciled with financials: sometimes due diligence checks that the money raised matches shares issued, etc. If you raised a prior round, have the bank statement or record of that cash coming in and the proper share issuance. Any outstanding loans or liabilities should be listed. If you have gotten any government grants or incentives (e.g. from Ignite or NIC), include documentation of those.

- You have proper financial statements (even if just management accounts for early-stage).

- Tax registrations (National Tax Number, Sales tax registration if needed) are in place.

- Past tax returns filed (income tax, withholding tax statements, etc.). Investors don’t want to inherit a tax mess.

- Cap table reconciled with financials: sometimes due diligence checks that the money raised matches shares issued, etc. If you raised a prior round, have the bank statement or record of that cash coming in and the proper share issuance.

- Any outstanding loans or liabilities should be listed.

- If you have gotten any government grants or incentives (e.g. from Ignite or NIC), include documentation of those.

In summary, a thorough due diligence covers corporate structure, IP, contracts, regulatory compliance, and financial health . “It should examine the startup across areas such as corporate structure, intellectual property, contractual obligations, regulatory adherence, and financial compliance” . As a founder, the best approach is to create a checklist and collect all these documents in one place (a secure cloud folder or data room). This not only speeds up the investor’s process but also gives you a chance to identify and fix any gaps beforehand.

Some practical steps to be ready:

- Conduct your own mini-audit: Imagine you are the investor – review your incorporation status, your contracts, IP, and compliance. Resolve any obvious gaps (e.g., if a key developer never signed an IP assignment, get it done before due diligence).

- Organize your data room: Have folders for legal documents, corporate records, financials, etc. Clearly label files. It makes you look professional and investor-ready.

- Be honest and transparent: If there is a known issue (say, a small dispute or a regulatory uncertainty), it’s better to proactively disclose it with an explanation of how you’re addressing it, rather than an investor “discovering” it later. Transparency builds trust.

Common Legal Mistakes Startups Make (and How to Avoid Them)

Throughout this guide, we’ve hinted at many mistakes to avoid. Let’s compile some of the most common legal pitfalls for startups preparing for fundraising, so you can ensure you’re not caught by these:

- Procrastinating Legal Formalities: Many founders delay incorporating the company, formalizing agreements, or handling legal paperwork, thinking it can wait. This often leads to chaos later. Avoid this by setting up your legal structure early and keeping it up-to-date. For instance, not incorporating and then having to scramble to issue shares to founders and early investors retroactively is messy and can spook investors (it’s listed as a fatal mistake by many experts). Similarly, not adopting basic corporate governance (bylaws, board meetings) is an oversight – “skipping proper corporate governance is not just a formality; it’s a mistake that can hurt credibility”.

- No Written Founder Agreement: As discussed, failing to have a clear founder agreement is extremely risky. So is not vesting founder equity. This is cited as one of the “most common and devastating mistakes” – it can lead to nasty splits and scare off investors who see unresolved founder issues. Solution: Draft that co-founder agreement early and include vesting, roles, dispute resolution, etc. (If you’ve been operating without one, it’s never too late to put one in place – better before an investor gets involved).

- Unassigned or Unprotected IP: Overlooking intellectual property is a critical mistake. Examples include: forgetting to have a departing co-founder or contractor sign IP over, using a name without checking trademarks, or writing code using someone else’s IP without license. These can derail funding (investors fear legal battles). Solution: Conduct an IP audit. Make sure every piece of key IP (code, designs, inventions) is owned by the company – get those assignment agreements signed. File trademarks for your brand/product names (so you can show investors you own the brand). If you have patentable tech, consider at least a provisional patent filing before fundraising (investors will ask if you have any patents). Essentially, secure your IP and document it.

- Messy Cap Table & Equity Promises: We’ve covered cap tables – a common mistake is poor cap table management. This includes not documenting equity splits properly, making verbal promises of equity to early hires or advisors and not formalizing them (leading to disputes), or losing track of convertible instruments. One law firm aptly calls poor cap table management a “deal killer”. Solution: Maintain a single source-of-truth cap table. Every equity-related event goes in it. If you promised someone equity, either formalize it (issue shares or options) or clarify it before an investor uncovers a claim. Use cap table software or at least review your spreadsheet with your lawyer periodically.

- Neglecting Legal/Regulatory Compliance: Young startups sometimes ignore things like registering for taxes, paying annual fees, or complying with labor laws, thinking they’ll fix it later. This can backfire in due diligence. For example, not filing your annual return with SECP or not paying a required tax can result in penalties or even put your company in bad standing. Solution: Even if you’re small, comply with the basics: file your annual accounts/returns, pay any government dues, maintain proper accounting. It’s worth consulting an accountant or company secretary to ensure you’re meeting statutory requirements. The cost of non-compliance can be far greater (fines or delaying a funding round to clean up the mess).

- Signing Bad Contracts Without Review: In the early hustle, founders might sign leases, loan agreements, or partnership MOUs without proper legal review. Some terms could haunt you (like a personal guarantee on an office lease, or an unfavorable exclusivity with a partner that limits future business). Solution: Get legal eyes on any important contract. If you can’t afford a lawyer for everything, at least read contracts carefully and watch out for onerous clauses. When in doubt, don’t sign something you don’t fully understand. Investors will look at key contracts, so you don’t want surprises (e.g., an investor finds out a “partnership” you signed actually gives away IP or revenue share that hurts your valuation).

- Not Understanding Investor Terms: Founders might be so eager to get funded that they accept tough term sheet clauses without realizing implications (like multiple liquidation preferences, supervoting shares for investors, overly restrictive covenants, etc.). These can later strip founders of control or upside. Solution: Educate yourself on common term sheet terms before negotiating. Lean on experienced mentors or lawyers to review term sheets. It’s easier to negotiate balanced terms upfront than to change them later. For instance, giving away a board majority or blanket vetoes to investors in Seed stage could hamper you – be thoughtful and don’t be afraid to push back on extreme terms. Many resources are available (YC, blogs) explaining what is “standard” at each stage.

- DIY Legal Work & Delaying Hiring Counsel: Trying to save money, some founders download random templates from the internet or postpone hiring any lawyer until things blow up. The Faison law group noted that waiting too long to engage legal counsel often means paying more later to fix preventable issues . Solution: While you should be frugal, legal is not a place to completely skimp. At minimum, have a startup-savvy lawyer do an initial setup (incorporation, basic agreements). Many lawyers will defer fees or do a fixed package for early startups. Use reputable templates if you must (e.g., YC’s SAFE, or industry-standard term sheets) rather than reinventing the wheel. And certainly by the time you are raising significant money, have a lawyer to guide you. It will actually save you money and headaches by preventing mistakes.

By avoiding these common pitfalls, you significantly increase your chances of a smooth fundraising journey. Remember, every startup makes some mistakes – the key is to proactively address them. As the saying goes, “an ounce of prevention is worth a pound of cure.” Laying a solid legal foundation might not feel as exciting as building product or signing customers, but it will pay dividends when that term sheet arrives and due diligence begins.

Final Thoughts: Building a Legally Solid, Investor-Ready Startup

Achieving fundraising success isn’t just about the pitch and the product-market fit – it’s also about inspiring investor trust through your startup’s legal hygiene. By following this legal checklist – from proper incorporation and founder agreements to maintaining a clean cap table and due diligence docs – you demonstrate that your startup is well-governed and ready for growth. Investors in 2025 are more diligent than ever, and they favor founders who are proactive about compliance and risk management. Think of legal readiness as insurance for your deal: the fewer surprises, the faster and smoother your funding round will close.

Finally, you don’t have to do this all alone. PakLawAssist is here to help Pakistani startups prepare for investor readiness. From providing legal drafts and guidance on local compliance (SECP filings, tax registrations, etc.) to reviewing your shareholder agreements or setting up an ESOP, PakLawAssist can support you at each step. We specialize in startup legal needs – ensuring your documentation is in order and spotting issues before investors do. With professional help, you can avoid costly mistakes and focus on building your business.

Call to Action: Reach out to PakLawAssist to schedule a startup legal readiness review. Whether you’re gearing up for a seed round or a Series A, our experts will help you compile your legal checklist, fix any gaps, and give you peace of mind when talking to investors. With the right legal foundation, you can fundraise with confidence – and turn your startup vision into reality.

Empower your startup with legal diligence today, and unlock investor funding tomorrow. Good luck with your fundraising journey!

Need practical legal support?

PakLawAssist's Legal Toolkit is built for founders, SMEs, and legal teams that want faster drafting, clearer compliance workflows, and more confident legal operations.

Visit the Legal Toolkit